Market Advisory

Must-See Information

The supply chain management and logistics industries move quickly. Our team provides time-sensitive and urgent information about conditions affecting markets around the world. Read more by clicking on one of the stories below.

Mitigating Risk: Planning for VUCEM System Outage

The Mexico Tax Administration Service recently announced that it has scheduled a maintenance outage to the Ventanilla Única de Comercio Exterior Mexicana (VUCEM) system, beginning on February 8th at 12:00 (Mexico-CST) that could last up to 7 days through February 15th...

Trade Policy: Key Strategies for Being Proactive in the Face of Potential Tariffs

Following President Trump’s announcement of tariffs on Canada, Mexico, and China, customs brokers and importers should be prepared to mitigate potential disruptions and financial impacts that increased duties could bring. Even if negotiations between the trade...

A Closer Look: Will Trump’s 25% Tariffs Be Implemented?

On Saturday, February 1st, the Trump administration imposed tariffs targeting Canada, Mexico, and China under the International Emergency Economic Powers Act (IEEPA). As a means to address the threat of illegal aliens and drugs, the tariffs include a 25% tariff on...

The ILA Strike Has Been Suspended

The 72-hour strike at two of the four terminals at the Port of Montreal ended as scheduled at 7 am Thursday, October 3rd. While operations recover from the work stoppage, companies waiting to import or export goods can expect some delays in the coming weeks. It is...

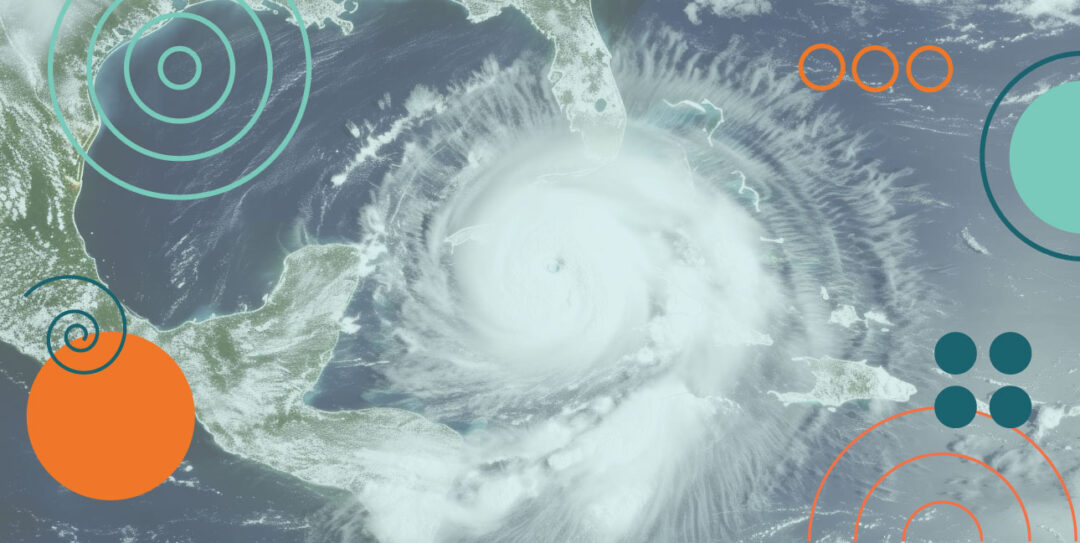

Hurricane Helene Leaves Behind Power Outages, Closures, and a 500-Mile Path of Destruction

September 27, 2024 Hurricane Helene Causes Power Outages and Closures Hurricane Helene officially made landfall at 11:20 pm in the Florida panhandle as a Category 4 Hurricane, causing fatalities and a path of destruction as it moved north. Helene weakened over land...

Looming Port Strikes Are on the Horizon Throughout North America

Shippers across the globe have been keeping a close eye on ports in North America, particularly labor negotiations between key unions and the ports. For months, the attention has been on stalled negotiations and a looming strike across the East Coast and Gulf Coast...

Strike Notice Issued as Negotiations Continue in Canada

The existing contract between the Teamsters Canada Rail Conference (TCRC) and rail-operating employers, Canadian National (CN) and Canadian Pacific Kansas City (CPKC), expired at the end of last year. Following several unsuccessful labor negotiations, the...

Adjustments of Customs User Fees for FY2025

We would like to inform you about an important update from U.S. Customs and Border Protection (CBP) that may impact your operations. On July 22, 2024, CBP published a general notice in the Federal Register announcing the adjustment of certain customs user fees for the...

Facing Unexpected Disruptions – Resilience in the Port of Baltimore

In light of the recent maritime tragedy at the Port of Baltimore, we would like to provide an advisory regarding its potential effects on supply chains, particularly on a national level. Overview: The recent incident involving a Maersk-operated vessel colliding with...

March 2024 Updates on the Global Supply Chain

With one step forward in the global supply chain, other issues and unforeseen disruptions cause additional challenges. GDL and DB Come to an Agreement The German Train Drivers’ Union (GDL) and Deutsche Bahn (DB), the national train operator, reached an agreement...